As we wrote recently, now is no time to “wait and see”. It is a moment of rapid, unsettling change for American civil society, especially the social sector. Mobilizing a response requires philanthropic leaders to play a role that their institutional contexts equip them well for: taking risks, doubling down to support grantees and communities facing an uncertain policy landscape. However, real risks loom; the wrong investments could waste resources at a time when opportunity costs are high. Great programs facing drastic public funding cuts could end without adequate resources.

But we also know, through experience and survey research, that foundations don’t behave exactly as theory would suggest. Over the years, we have analyzed survey results from hundreds of foundation program officers to understand how they view risk. Social sector leaders face the same cognitive biases as all decision-makers, especially risk aversion (favoring guaranteed options over potentially better but uncertain options) and loss aversion (fearing bad outcomes more than desiring good ones).

Since the status quo feels less risky than acting in the face of uncertain and potentially negative outcomes, decision-makers can be tempted to delay or avoid making hard decisions. This is why “wait and see” as an orientation is so tempting, even though it may be the product of cognitive biases, not rational planning. As we outlined in ‘Our Unprecedented Opportunity in 2025’, foundations that can move beyond this paralysis can catalyze transformative change. The approach presented here provides the concrete methodology to transform the big-picture strategic imperatives of this moment into actionable decisions.

The way through is rapidly and rigorously identifying the “trunk” of a tree with many branching scenarios. What grantmaking approaches are crucial under any likely scenario? And what grantmaking approaches are less exposed to the uncertainties that shape the branching scenarios? These investments form a no-regrets “trunk” that makes the branching scenario response even more powerful.

Risk and change can knock us into patterns of thinking that are instinctive and emotional, and prone to cognitive biases (System 1 thinking as defined by Amos Tversky and Daniel Kahneman). Taking the right risks requires us to shift instead into System 2 thinking – deliberative and logical. System 2 thinking can require more energy, more focus, and more time, though a structured approach can help.

In this piece, we offer a structured approach to cut through the uncertainty, informed by modern portfolio theory and 20 years of guiding social impact strategy. Ultimately, we aim to empower philanthropic leaders to act decisively despite uncertainty.

A Framework for Assessing Portfolio Risk

Section Summary: Risk assessment begins by understanding how your foundation’s investments are interconnected. This section provides practical tools to understand risk so that no-regrets actions become clearer. We outline three steps: chart interdependence across theories of change, analyze relationships between specific investments, and assess exposure to external factors. Together, these steps help create a comprehensive risk profile that reveals both vulnerabilities and opportunities.

Finding no-regrets actions under uncertainty depends on understanding correlation in outcomes and opportunities for diversification. As Shakespeare’s Antonio declared, “My ventures are not in one bottom trusted / Nor to one place; nor is my whole estate / Upon the fortune of this present year.” Antonio diversified across ships to minimize the risks of storms, across places to minimize the risks of politics and markets, and across time to minimize the risks of disruptions by climate or disease.

Diversification requires analyzing correlations – the degree to which the successes and failures of investments are related to each other, either because they are interconnected or because they share exposure to common outside risks1.

Like Antonio diversifying to mitigate ship-based, place-based, and time-based risks, foundations can diversify to mitigate against risks to specific grantees, risks that undermine whole theories of change, and the uncertainties that can affect them all.

Portfolio interdependence

Foundations’ theories of change often connect in ways that aren’t immediately obvious. Consider a regional foundation with these two investment theories:

- Theory A: If we support trauma-informed mental health services in our region’s schools, it will lead to improved student emotional regulation, which will advance academic achievement and graduation rates in our region.

- Theory B: If we support living-wage workforce development programs with industry partners in our region, it will lead to increased family economic stability and reduced housing insecurity, which will advance intergenerational economic mobility in our region.

While seemingly independent (one focuses on students, one on adults), these theories are likely interconnected: the adults in Theory B may be parents of students Theory A, and students in Theory A may grow up to become the adults in Theory B. Success in each theory creates better conditions for the other, while failure creates additional barriers.

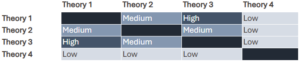

Foundation leaders can assess interdependence with a simple matrix using a scale of Low, Medium, and High.

Table 1: Interdependence across theories of change

In this example, Theories 1 and 3 are highly interdependent, Theory 2 is moderately interdependent with Theories 1 and 3, and Theory 4 is relatively independent. Overall, this foundation is striking a careful balance between diversification (i.e., not all theories are highly interdependent with each other, which reduces risk) and synergistic planning (i.e., Theories 1-3 work in tandem with one another, which increases synergies but also increases risk).

Beyond cross-theory connections, interdependence also exists within theories of change. For example, if one area of grantmaking within a program focuses on research and pilots, while another scales working ideas, research failures will create a weak pipeline and no scaling opportunities.

For each theory of change, foundations can generate a list of major investments, and then assess within-theory interdependence using these ratings:

1 = Any of the investments could succeed even if all the others failed

2 = Most of the investments could succeed even if the others failed

3 = Some of the investments could succeed even if the others failed

4 = Most of the investments will either succeed or fail together

5 = All of the investments will either succeed or fail together

We have found the easiest way into this analysis is to consider what would happen if a handful of the most important investments in the portfolio failed for any reason – say an isolated leadership failure within the grantee. What would happen to other key investments? And the overall impact of the grant portfolio? By considering conditional probabilities, the probability of one event (failure) given a specific outcome of another uncertain event, we can both unpick complicated relationships between grants, and establish the basis for additional quantitative analysis (if helpful).

Table 2: Interdependence within theories of change

This analysis reveals that Theory 2 has the most interrelated investments, increasing its internal risk profile. However, as we saw in Table 1, Theory 2 has at most a “medium” level of interdependence with other theories.

Note: Time permitting, a more comprehensive version of the analysis in Table 2 would require first creating interdependence matrices for the investments within each theory of change before summarizing the results at the theory of change level.

External Risk Exposure

Portfolio correlation (and thus, risk) is also driven by shared exposure to external risk factors. Foundation leaders should identify 5-10 relevant risks from categories such as:

- Political (shifts in government priorities or leadership)

- Legal (laws that restrict activities or funding mechanisms)

- Economic (market volatility, economic downturns, inflation)

- Cultural (shifting public attitudes, reputational factors)

- Environmental (natural disasters, resource scarcity)

- Technological (emerging technologies, cybersecurity threats)

- Organizational (staffing changes, leadership transitions, budget fluctuations at key grantees)

- Other (public health crises, global conflicts)

After listing key risks, foundation leaders can assess their probability (as a percentage) and potential impact on each theory of change, using these ratings:

1 = Negligible impact

2 = Slightly harder/less likely to succeed

3 = Moderately harder/less likely to succeed

4 = Significantly harder/less likely to succeed

5 = Existential threat to this work

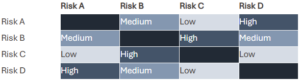

Table 3: Shared exposure to outside risk factors

This assessment reveals that Theories 1 and 2 share exposure to Risk A, which would pose an existential threat (5) to both investment areas if it occurred, and to risk B, which would make it significantly harder (4) for both theories to succeed. Though the probability is relatively low (15-20%), the severity of these risk factors warrants serious attention. This shared vulnerability could undermine half of the foundation’s theories of change simultaneously.

It is important to recognize how external risks and interdependencies within theories of change interact. For example, any external risk that impacts theory 2 is more dire, all else equal, because theory 2 has the most internal interdependencies. Furthermore, theory 2 has implications for theories 1 and 3; carefully monitoring Risks A and B for how they are affecting theory 2 (and therefore theories 1 and 3) is likely effort well spent.

Note: Time permitting, more comprehensive version of the analysis in Table 3 would require first evaluating the impact on each individual investment within a theory of change before summarizing at the theory of change level.

Portfolio Risk Summary

When all three analyses are combined—cross-theory interdependence, within-theory interdependence, and external risk exposure—a comprehensive risk profile emerges. In the example tables above, the portfolio carries relatively high risk, with three of four theories highly correlated through a combination of interdependence and shared external risk exposure.

This interconnectedness creates both opportunities and vulnerabilities. The high internal correlation within Theory 2 (rated 4 out of 5) indicates that its component investments are designed to work together synergistically, with most expected to succeed or fail as a unit. While this approach maximizes potential impact if successful, it also increases vulnerability—one weak link could compromise the entire theory. Meanwhile, the foundation’s relatively independent Theory 4 provides some portfolio stability, as it operates with limited exposure to the risks that threaten other investment areas.

For foundations conducting similar analyses, patterns to watch for include over-reliance on a singular path to impact (high within-theory correlation across multiple theories), multiple theories vulnerable to the same external threats, limited independence among theories (few “low” interdependence ratings), and concentration of existential threats. These patterns signal excessive portfolio correlation and suggest a need for strategic risk management through the approaches outlined in the following section.

Strategic Approaches to Managing Risk

Section Summary: Once you understand your impact portfolio’s risk profile, you can find the “trunk” that represents a no-regrets path forward. This section outlines three complementary strategies that often represent no-regrets moves: increasing diversification across less correlated investments, building general resilience capabilities that work across multiple scenarios, and developing targeted action plans for specific, high-impact risks.

Once foundation leaders understand their portfolio risk, they can pursue risk management approaches that are either scenario-agnostic or scenario-specific. These approaches help activate System 2 thinking by providing structured frameworks for deliberative decision-making in the face of uncertainty.

- Increase Diversification

Diversification remains a foundational risk management strategy in both financial and social impact portfolios. Foundation leaders should consider reallocating resources to theories of change that are less correlated with the rest of their portfolio, and/or reallocating investments within theories of change to specific investments that could succeed even if the rest of the investments in the theory of change failed. For example, a foundation focused on advancing student educational outcomes could increase diversification through supporting both in-school and out-of-school programs, funding work in multiple geographies with different policy environments, and investing in both shorter-term direct services and longer-term policy advocacy.

By intentionally spreading resources across less correlated investments, foundations can reduce the likelihood that a single risk event will compromise their entire portfolio.

- Build General Resilience

Beyond diversification, foundations should invest in general resilience capabilities that work across multiple future states. As we noted in our analysis of preparing for the new administration, building strong networks across sectors and geographies ensures support systems remain intact during crises. This includes:

- Streamlining internal foundation processes to enable faster decision-making

- Building relationships with values-aligned funders to work collectively

- Identifying or creating funding vehicles (e.g., pooled funds) that can efficiently and flexibly deploy resources

- Strengthening key partners’ security (cyber and physical) and financial stability

- Funding field networks across sectors and geographies to ensure support systems remain intact during crises

- Develop Scenario-based Action Plans and Identify Scenario-independent Opportunities

For more targeted risk management, foundations should engage in scenario planning focused on specific risk clusters. This approach is particularly valuable in responding to the policy shifts we’re currently witnessing. For example, clients working in education, climate, human services, and democracy are actively using scenario planning to prepare for both immediate impacts and longer-term structural changes in their operating environments.

We recommend starting by using a matrix to assess relationships between risks using a simple scale: Low, Medium, and High. This matrix helps identify which risks tend to manifest together, creating compound challenges that require coordinated responses. Those clusters of related risks can then become key scenarios.

When creating this correlation matrix, focus only on risks that have moderate to severe potential impacts (impact ratings of 3 or higher from your earlier assessment). Risks with minimal impact (ratings of 1-2) generally don’t warrant detailed scenario planning, regardless of their probability. This focused approach ensures your scenario planning addresses consequential risks without becoming unwieldy.

Table 4: Correlations between risks

Strong relationships between risks form the basis for scenario development. In this example, we might create one scenario around risks A and D, and another around risks B and C.

For each risk cluster, develop a detailed narrative that describes:

- How correlated risks might unfold together and amplify each other

- Key indicators that would signal the scenario’s emergence

- Potential cascading effects beyond direct impacts

For each priority scenario, foundations should:

- Identify early warning signs of the scenario to monitor

- Develop immediate steps to reduce the likelihood of the scenario, if not already covered under Build General Resilience

- Consider ways to build redundancy into affected theories of change (see Tables 1-3) to make it less vulnerable to the scenario (e.g., funding multiple organizations with overlapping missions in case one organization is the subject of politically motivated attacks)

- Build scenario-specific resilience (e.g., establish legal defense funds, crisis communications resources)

- Create detailed plans for how to respond to the scenario if it occurs (e.g., pre-approved emergency grant processes, rapid decision-making protocols, pre-drafted communications templates, pre-established partner coordination mechanisms, criteria for shifting resources between theories of change, guidelines for suspending or accelerating specific investments)

That last step – detailed planning by scenario – also points to the investments that make sense under any scenario. These, along with investments that aren’t exposed to any of the key risks, can become your no-regrets “trunk” at the base of branching scenario responses.

Remember, the goal of these approaches is not to predict the future with certainty. Rather, it’s about becoming a more responsive, prepared organization that can maintain focus on long-term goals even as conditions change. Regularly revisit and refine both your general diversification and resilience measures and your scenario-specific plans as new information becomes available and as the risk landscape evolves. And this qualitative work can also form the basis for more detailed quantitative analysis.

Moving Forward: From Theory to Impact

Section Summary: The tools shared here help philanthropic leaders shift from reactive to deliberative thinking when confronting uncertainty. By embracing these portfolio management approaches, foundations position themselves to not only weather unexpected shifts but also capitalize on emerging opportunities. Striking that balance advances foundations’ dual responsibility to preserve long-term capacity while effectively addressing society’s most pressing challenges.

The approaches outlined here provide a starting point for foundations seeking to strengthen strategic decision-making in an increasingly complex and uncertain world. These frameworks help philanthropic leaders move from System 1 thinking (reactive, instinctive) to System 2 thinking (deliberative, logical) when confronting risk—making them less susceptible to the cognitive biases that can lead to “wait and see” paralysis in turbulent times.

As sector boundaries continue to evolve and social challenges grow more interconnected, the ability to build resilient, adaptive portfolios becomes essential. Foundations that embrace these portfolio management approaches will be better positioned not only to weather unexpected shifts but also to capitalize on emerging opportunities. This balanced focus on both risk mitigation and opportunity capture reflects the dual responsibility of philanthropic institutions: to preserve their capacity for long-term impact while boldly addressing society’s most pressing challenges.

The field of philanthropy has an opportunity to develop its own distinctive approach to portfolio theory—one that acknowledges the unique characteristics of social change investments while drawing on the best insights from financial markets. For example, interconnectedness in a portfolio can intensify risk, but interconnectedness in the social sector can be a source of solidarity, strength, and impact. By sharing learnings across institutions and refining these methods, foundations can collectively strengthen their ability to deploy resources for maximum social benefit in an uncertain future.

At Redstone, we’re working alongside our clients to apply these frameworks in real time as they navigate both the challenges and opportunities of this pivotal moment. We invite you to track our series on how to seize the unique opportunities 2025 presents.